At the start of each calendar year, we like to take the time to identify what themes & opportunities (T&Os) have the potential to contribute to performance for the upcoming 12 months. These T&Os may already be playing out, or we may be waiting for further developments and evidence prior to introducing these T&Os into a portfolio.

A selection of these are detailed below:

-

Long equities

After equities experienced a year of very positive performance in 2019, you may be foolish to think that 2020 will be year where equities cool off. Are valuations high? Yes. Are equity markets at all-time highs? Yes. Has growth slowed? In most regions, yes. Despite this, we currently have synchronised easing of monetary and fiscal policy from global central banks in an attempt to ‘reflate’ the global economy. The quote by Marty Zweig ‘Don’t fight the Fed’, is more accurate today than ever. Money is cheap, which means investors are continually looking for a home for their money, rather than holding cash. We are not saying that there won’t be volatility during 2020, or that you should be buying equities at any price. However, if global central banks continue with their current stance of cheap money, equities should outperform. This T&O currently exists.

-

Long base metals

Following on from the above reflation trade thematic, as global central banks attempt to reflate the global economy through both monetary (low interest rates) and fiscal policy (government spending), we expect to see a rebound in global growth. If a rebound does occur, investments in base metals (copper, tin, zinc) that are associated with growth should experience an increase in demand. We believe that price leads fundamentals in the majority of instances, therefore, by looking at the copper price, we see signs of life. This T&O is developing.

-

Rebound in Hong Kong equities

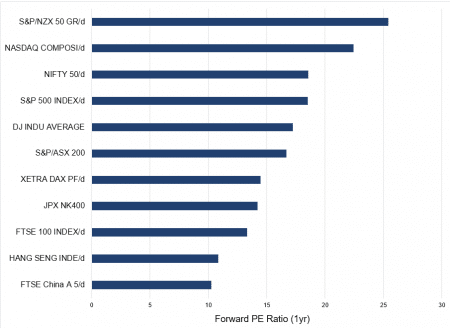

Continuing from T&O number 1, we are bullish global equities but at the right price. The Hong Kong share market (Hang Seng) was beaten up over the last 12 months, with political uncertainty, riots and trade wars dragging on performance. From a valuation perspective, the Hang Seng currently trades on a 1-year forward price to earnings ratio of 10.9x vs the S&P 500’s 18.4x. Indeed, there is additional risk priced into the Hang Seng, however at some point, investors may view the Hang Seng as better value than buying United States (US) equities on stretched valuations. In 2020, investors may look for better valued areas to allocate their money. This T&O is developing.

-

Election opportunity

This year we have the US election, which is bound to provide some opportunities for investors to consider. Analysing the last 14 US election years, average returns are 7.36% with annualised volatility of 11.87%. Excluding 2008, returns are 10.88% and volatility is 10.68%. This is compared to the average annual returns of 7.88% and average volatility of 13.63% for the S&P 500 for the last 55 years. By excluding the outlier event of the GFC, returns seen during election years are generally better than average, and with lower volatility. Historically, November is a good month for equities with an average return of 0.85%, however during election years average monthly returns increase to 1.35% (excl. ’08). Considering how much equities have already moved over the last year, we expect there to be profit taking and global events that may result in sell-offs, however taking the above into consideration, our bias is net long. This T&O is developing.

-

Battery metal turnaround

During 2019, we saw battery metal producers in a sector-wide downtrend. GXY, ORE, PLS and SYR were down 57%, 18%, 55% and 68%, respectively. This was due to an oversupply in lithium and graphite, which resulted in a decline in prices. Recently, an inflection point has been reached on the demand side. Investors have become extremely bullish on Tesla’s electric vehicle and battery market demand forecast. This has ignited a share price rally from $299.68 to $537.92 (79%) upon release of their most recent earnings report on 24/10/19. This exuberance has flowed back down the supply chain to battery metal producers. GXY, ORE, PLS and SYR are up 52%, 63%, 39% and 80% respectively, from 24/10/19 to 14/01/20. The T&O is currently playing out but will require further evidence to suggest the demand and subsequent share price moves are sustainable.

I’d encourage investors to get in touch at our office to discuss these themes further.