Weekly Update | December 15, 2023

Let’s hop straight into five of the biggest developments this week.

1. US Federal Reserve left rates at 5.50%

The FED left interest rates static at 5.50% for the third successive meeting, a move well anticipated by markets. The fall in headline inflation underpinned the unanimous decision that was accompanied by a softer than usual statement. The central bank indicated for the first time that it would pivot towards rate cuts next year, giving the clearest pointer yet that its most aggressive tightening policy since 2001 is finally coming to an end.

2. Australia’s unemployment rate rose to 3.9%

The Australian labour market suffered a fresh blow after unemployment rate rose faster than initial estimates. Unemployment rose to 3.9% in November, the highest in one and a half years, and overshooting the previous 3.8% mark that markets had bet on retain. This was despite a surge in employment change, attesting to the fact that high-interest rates and a struggling economy are having an impact.

3. Switzerland kept interest rates static at 1.75%

The SNB sat in its hands to leave interest rates unchanged at 1.75% for the second consecutive meeting. Inflation indicators point to a significant waning of inflationary pressure, while economic growth in the third quarter remained weak. The central bank, however, indicated a reversion to a data-driven approach to guide its monetary policy going forward, indicating readiness to respond accordingly to future developments.

4. UK maintained interest rates at 5.25%

The BOE maintained its official bank rate at 5.35%, in line with market expectations. In a 6-3 majority decision, the central bank appeared unyielding to any prospects of a possible cut in the near future. The implication was that the BOE is angling towards a higher for longer approach to attain its inflation objective after its economic projection pointed to elevated Inflationary pressure in the medium term and that there is still some way to go in addressing it.

5. ECB held interest rates steady at 4.5%

The ECB put its monetary tightening policy on hold for the second time in a row, maintaining its main refinancing rate at 4.5%. The move was in line with market anticipation after a sharp fall in inflation for the entire Eurozone block. The decision is further reinforced with weaker than expected growth, with the central bank going further to revise its growth forecasts lower.

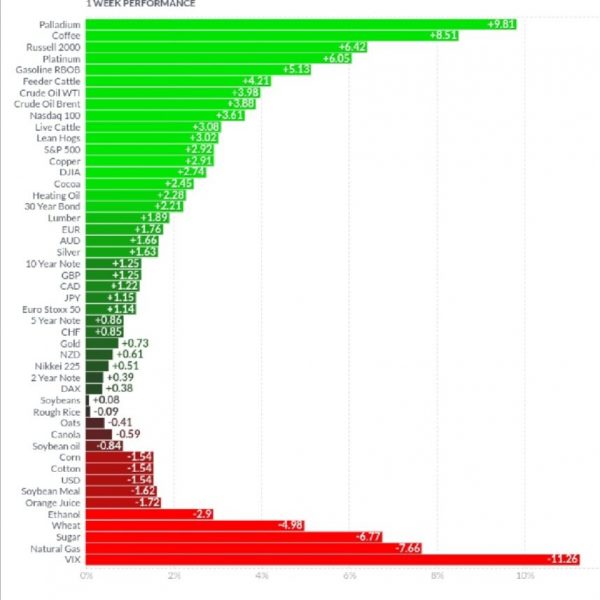

As per usual, below shows the performance of a range of futures markets we track. Some of these are included within the universe of our multi-strategy hedge fund.

The energy complex rebounded markedly as producers escalated their supply cut measures to mop up surpluses while the weakening dollar injected respite from weeks of relentless declines. Moreover, demand began to emerge after US crude stockpiles dropped by a staggering 4.3 million barrels. Gasoline BROB and crude oil were up 5 1% and 3.98% respectively. Palladium rallied on supply fears after South African mine workers rejected a pay rise deal with the country being the world’s chief producer. Coffee remained up on seasonality while sugar, natural gas, ethanol, and wheat sold off on oversupply. The VIX tumbled sharply on speculation that the Fed had finished with its monetary tightening policy, leaving the door open for rate cuts in 2024, a fundamental that kept the dollar index muted. Investors were further enticed by the fact that Chinese authorities are currently working on a new round of stimulus packages to prop up the sluggish Chinese economy. Global indices rallied on peaking interest rates across the board as investors sort alpha in risky investments.

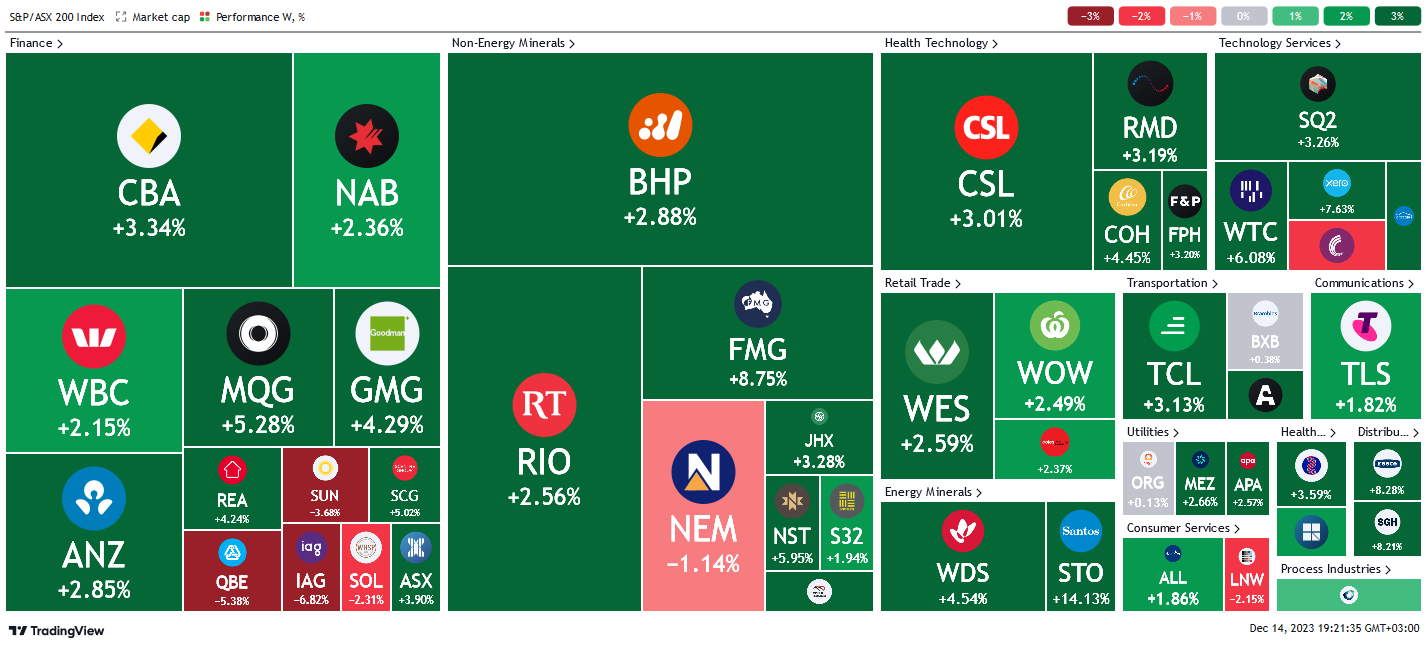

Here is the week’s heatmap for the largest companies in the ASX.

The ASX fired on all cylinders, extended gains from last week to close on a high. Financials led the charge with most stocks in the green as analysts anticipated interest rate peaks across the board. MQG and SCG were in overdrive, gaining +5.28% and +5.02% respectively. IAG and QBE were however among some surprise losers that outsold the index at – 6.82% and – 5.38% respectively. Non energy miners were all green in anticipation of capital flows from China’s new stimulus package. MIN and FMG were up a massive +9.02% and 8.75% respectively while NEM was the only decliner in the sector to close on a – 1.14% loss. Healthcare tech, tech services, retailers, transporters, and energy miners were all a sea of green without deviation or exceptions to wrap up a mega-bullish week.

Please reach out if you’d like to find out more about how our quantitative approach captures the price action covered above, or if you would like to receive these updates directly to your inbox, please email admin@framefunds.com.au.