Weekly Update | May 3, 2024

Let’s hop straight into five of the biggest developments this week.

1. Chinese Manufacturing PMI steady at 50.4

China’s factory activity remained in expansion territory for the second consecutive month in April, in the latest sign that the economic recovery is picking up pace. The focus from the Chinese government to expand their economy seems to be working in the short term after a period of 5 consecutive monthly declines.

2. US employment cost index rises 1.2% q/q

One of the most monitored readings by the US Federal Reserve beat expectations and rose by 1.2% q/q. This increase beat expectations of 1.0% showing that wages have continued to rise, which is not a good sign for the Fed if they want to see the labour market slowing. This reading caused the US market to decline aggressively mid-session.

3. US Job Openings decline to 8.49M

The number of job openings changed little at 8.5 million on the last business day of March. Over the month, the number of hires changed little at 5.5 million while the number of total separations decreased to 5.2 million. This data was somewhat conflicting considering the employment cost index beat expectations earlier in the week.

4. US Fed leaves rates at 5.5%

The US Federal Reserve held rates steady this week and Jerome Powell talked back expectations that they were going to be raising rates this year. He also reiterated that there is still more work to be done tackling inflation, however he expects that the path of rates in the near term will be lower vs higher.

5. Bank of Japan intervenes in currency markets

The Yen broke through the key 155 level earlier this week, which was a key level identified by the Bank of Japan and their Minister of Finance. The BOJ quickly sent out speakers to inform the market that they are monitoring FX moves and that they are ready to intervene. Within hours, the Yen declined as the BOJ intervened. These solutions seem to be very short term in nature, and if the BOJ really wants to change the trend, they will need to make a structural change to their stance on monetary & fiscal policy.

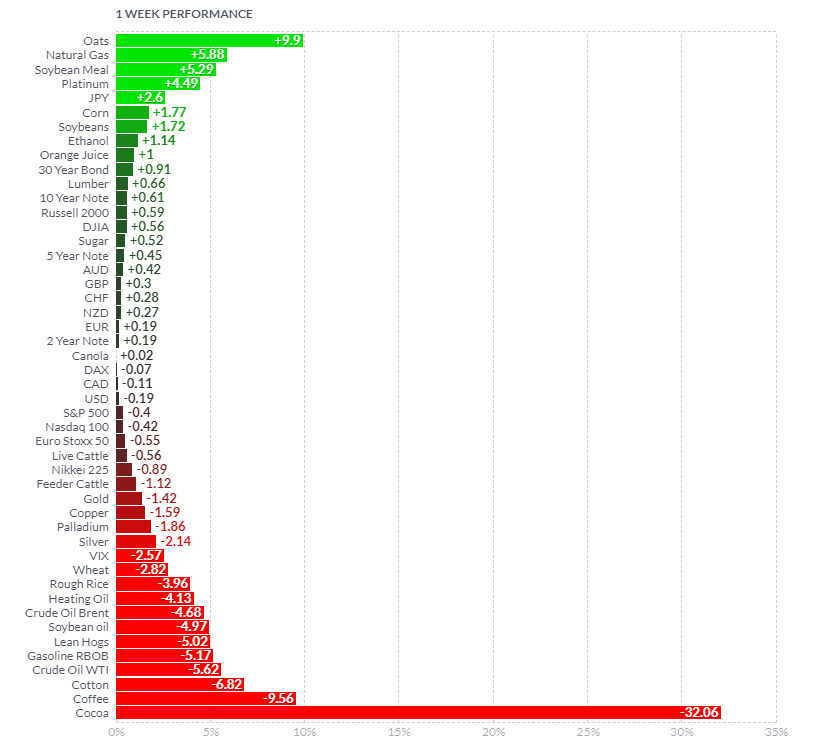

As per usual, below shows the performance of a range of futures markets we track. Some of these are included within the universe of our multi-strategy hedge fund.

The round trip in Cocoa has continued aggressively over the last week. Wetter weather conditions have caused Cocoa to sell off by -32% over the course of the week. It is worth noting that Cocoa is still up by 100% YTD. Coffee also continued to decline over the week due to better than expected growing conditions. Equities have been relatively flat over the week, however, have had some day-to-day volatility. The only bright spots over the week have been Natural Gas +5.82% and Oats up +9.9%, however, there have been no true catalysts driving this price action.

Here is the week’s heatmap for the largest companies in the ASX.

On the surface, the XJO has been flat over the week, however, underneath the surface there has been a large level of volatility in numerous large cap constituents. BHP has suffered over the week, down -6.03%, after they made a 31.2bn pound bid for Anglo America. FMG and RIO were up for the week, as iron ore prices were closed in China. The banks were moved with CBA, WBC, ANZ, and MQG all down, while NAB was the bright spot, up +0.53%. Utilities and industrials all experienced some selling as market participants repositioned after last week’s change in expectations for rate increases. Essentially investors had been buying up this part of the market for their yield, however, if expectations have shifted for further rate hikes, then a higher rate of return can be found elsewhere. Energies declined considerably, led by the oil price. WDS and STO were both down over -4%.

On the surface, the XJO has been flat over the week, however, underneath the surface there has been a large level of volatility in numerous large cap constituents. BHP has suffered over the week, down -6.03%, after they made a 31.2bn pound bid for Anglo America. FMG and RIO were up for the week, as iron ore prices were closed in China. The banks were moved with CBA, WBC, ANZ, and MQG all down, while NAB was the bright spot, up +0.53%. Utilities and industrials all experienced some selling as market participants repositioned after last week’s change in expectations for rate increases. Essentially investors had been buying up this part of the market for their yield, however, if expectations have shifted for further rate hikes, then a higher rate of return can be found elsewhere. Energies declined considerably, led by the oil price. WDS and STO were both down over -4%.

Please reach out if you’d like to find out more about how our quantitative approach captures the price action covered above, or if you would like to receive these updates directly to your inbox, please email admin@framefunds.com.au.