Weekly Update | February 02, 2024

Let’s hop straight into five of the biggest developments this week.

1. Chinese manufacturing PMI ticked up to 49.2

The post Covid-19 recovery in Chinese manufacturing remains on course, albeit with ebbing momentum. The manufacturing PMI edged higher to 49.2 from the previous 49.0, pointing to ongoing progress to expansion. This, however, undershot the more optimistic market expectation of 49.3. The deduction is that although current stimulus policies are having profound effect, more concerted effort is still required to attain sector growth.

2. Australia’s CPI slumped to 3.4% y/y

Inflationary pressure in Australia is cooling off ahead of schedule. CPI fell to 3.4% in the twelve months to December, a significant reduction from the previous 4.3%. The rate of inflationary deceleration was much faster than the 3.7% anticipated by markets. The inference is that the historically high interest rates are proving effective in pushing towards the RBA’s inflation target.

3. US employment cost index fell to 0.9% q/q

Employers are spending less than expected on labour in the US. The employment cost index receded to 0.9% from the previous 1.1% in the final quarter of 2023, lower than the market forecasts of 1.0%. The structural changes in the US labour market continue to manifest on employment costs as automation takes hold.

4. US FED held interest rates static at 5.5%

The US FED left the Federal Funds rate unchanged at 5.5%, in a move well read by market participants. With inflation on the wane, the central bank moved on from its tightening bias. Solid economic performance, however, saw the statement point to lack of urgency to cut rates too soon. The inference to markets was that a status quo of circumstances is emerging where a higher for longer short-term policy is preferred.

5. UK leaves interest rates unchanged at 5.25%

The BOE left its official bank rate static at 5.25% for a fourth consecutive sitting. The majority decision was in line with market expectations and was largely underpinned by an overall reduction in inflationary pressure. The voting outcome however points greater impetus to raise rather than cut rates, pointing to possibilities of holding the current 16-year high rates for longer.

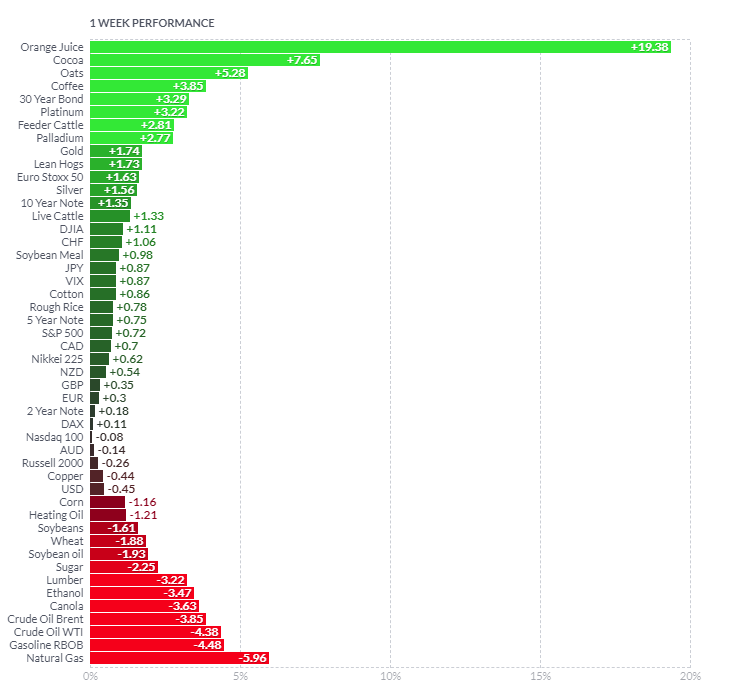

As per usual, below shows the performance of a range of futures markets we track. Some of these are included within the universe of our multi-strategy hedge fund.

A combination of unfavourable weather and bacterial infection has reduced orange output in Brazil, Mexico and USA, driving the price to an all-time high this week. Supply fears occasioned by the El Nino weather pattern has also constricted supply for cocoa, coffee and oats. The VIX chopped around over the week as markets whipsawed around the FOMC meeting and statement. Gold roared higher on geopolitical risk and uncertainty. The energy complex took a breather after a period of consistent price increases. Wheat, canola, ethanol and corn were dismal in a seasonally driven glut, as crop yields look to be higher than expected.

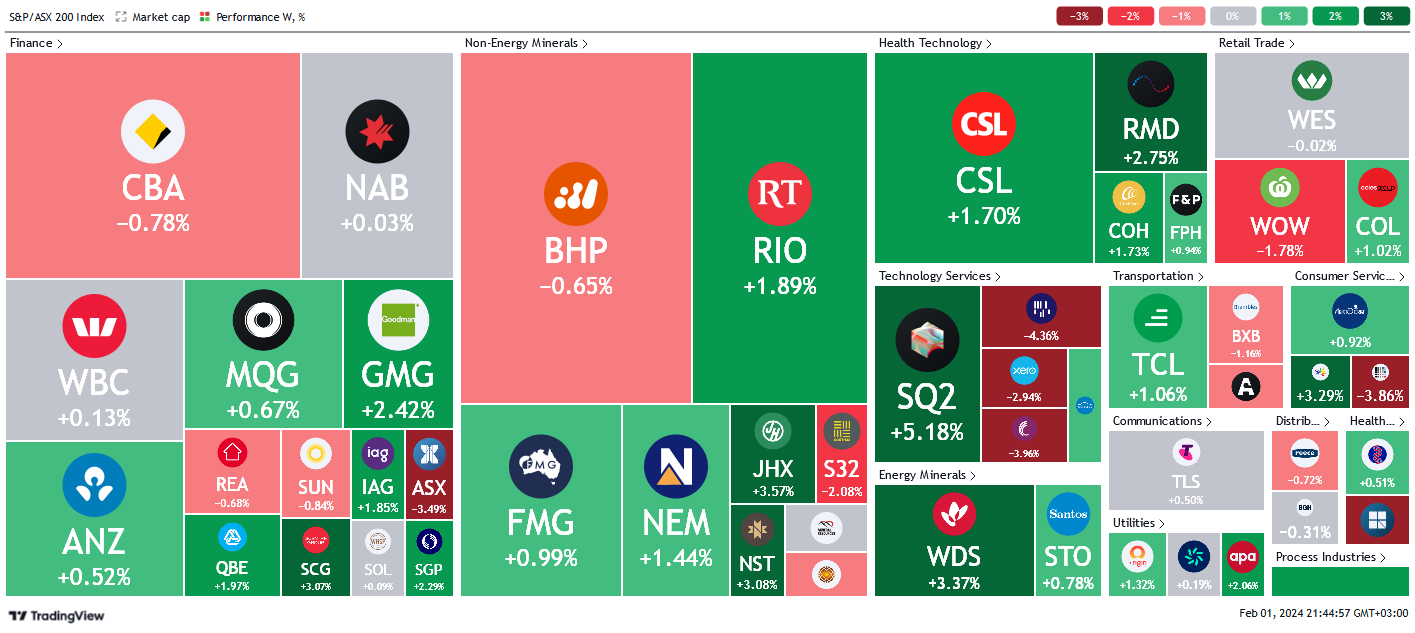

Here is the week’s heatmap for the largest companies in the ASX.

A mixed week for the ASX as markets weighs up cooling inflation and possibility of a rate cut; and adversities of geopolitical shocks. Financials were mixed with some stocks like SCG and GMG doing most weightlifting with impressive gains of +3.07% and +2.42% respectively. ASX was the biggest loser, closing – 3.49% down. Non energy minerals were similarly mixed albeit with a bullish bias. JHX and NST were the biggest gainers, netting +3.37% and +3.08% while S32 lost most at – 2.08%. Healthcare tech, consumer services and energy miners were green without exception. Tech services, retailers and transporters posted mixed results.

A mixed week for the ASX as markets weighs up cooling inflation and possibility of a rate cut; and adversities of geopolitical shocks. Financials were mixed with some stocks like SCG and GMG doing most weightlifting with impressive gains of +3.07% and +2.42% respectively. ASX was the biggest loser, closing – 3.49% down. Non energy minerals were similarly mixed albeit with a bullish bias. JHX and NST were the biggest gainers, netting +3.37% and +3.08% while S32 lost most at – 2.08%. Healthcare tech, consumer services and energy miners were green without exception. Tech services, retailers and transporters posted mixed results.

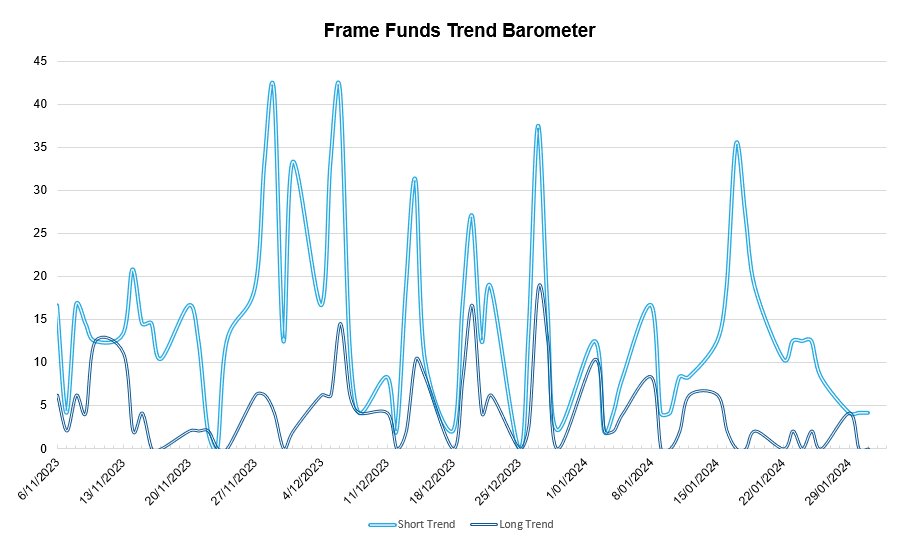

Below shows our proprietary trend-following barometer which captures the number of futures contracts within our universe hitting new short and long-term trends.

Please reach out if you’d like to find out more about how our quantitative approach captures the price action covered above, or if you would like to receive these updates directly to your inbox, please email admin@framefunds.com.au.