Over the last 18 months, we have experienced a draw-down of greater than 20% on the United States (US) equity markets, however recently they have reached a new all-time high. Australia has recaptured its 2007 high, whilst major European markets are also within touching distance of their all-time highs.

As an investor, there are a few questions that need to be researched when investing at all-time highs.

1. What are the characteristics of the market at index level at all-time highs?

2. What investments make sense at these levels?

3. How do we make investments with the information we have discovered from points 1 & 2?

1. What are the characteristics of the market at index level at all-time highs?

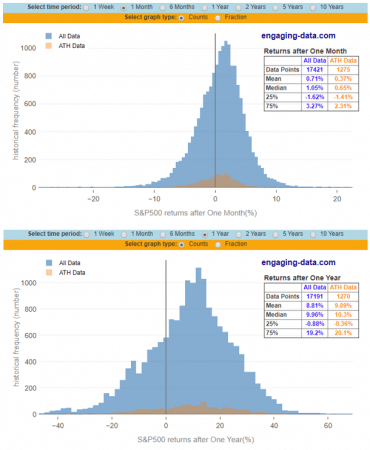

When analysing the S&P 500 from a return basis, the way an index trades at an all-time high is not too dissimilar from the market during any other period. The S&P 500 spends a good portion of the time at all-time highs. Data provided at engaging-data.com states that there have been almost 1300 days where the index was at an all-time-high, out of the more than 17000 market trading days since 1950. This implies that the market spends just under 8 percent of its time at all-time highs. Additionally, for over 36 percent of these days, the index is within 1 percent of the all-time high.

The distribution of returns after reaching an all-time high is extremely similar to the returns for all other days in the market. The following figures compare the two distributions of market returns after a period of one month and one year:

As an index captures all-time highs, generally there is an increase in the average true range (after a period of one month), or how many points the index moves per day. It is common for financial media to report changes in index values on an absolute, or point, basis rather than in percentage terms. This allows the media to claim titles such as “the largest point drop on record”; however, this is grossly misleading. Although the point changes are larger, they are often similar in percentage terms when comparing the returns to historical data.

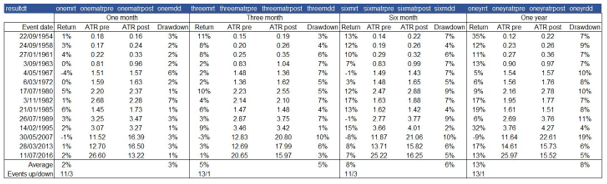

Drilling down, we have collected data from the S&P 500 to analyse market characteristics when the index makes a new high after a twelve-month period in which it fails to make a new high. There is a total of fourteen events that meet this criteria.

Below we analyse the forward returns, average true range (ATR) for the corresponding period pre and post the event date and the draw-down following the event date for the corresponding time period. The four periods are one, three, six and twelve months.

The forward return post these events is positively skewed. One-month forward returns show an average return of around 2%, with 11/14 instances positive. Three, six & twelve-month forward returns show 5%, 8% and 13%, respectively.

As mentioned above, the change in the ATR follows a logical pattern. As markets rise and the index expands, the ATR also expands. We note 11/14 occurrences show an expansion. Recently however, we have seen a contraction. This has been a recent characteristic of the low volatility grind higher which has coincided with the introduction of modern monetary theory and a rise in passive investment.

The average draw-down one, three, six and twelve months later is 3%, 5%, 6% and 8% respectively.

In simplistic terms, the reward to risk for one, three, six and twelve months later is 1.26, 1.38, 1.69 and 2.21, once again demonstrating a positive skew. We note that for one-month forward reward to risk there are 7/14 instances where the reward for $1 of risk is negative.

To summarise this data and interpret it when making simplistic investment decisions, taking new investments when an ATH is made is skewed positively, however the investments may experience some volatility in the short term. The reward to risk profile improves the longer the investments are made (twelve month forward reward to risk is 2.21:1 with 9/14 instances reflecting a reward to risk >1:1).

2. What investments make sense at these levels?

Investing at all-time highs is difficult, as the market tends to be far away from any sort of technical support and sometimes sound fundamentals. Additionally, if you do not rebalance your portfolio, some individual positions may grow at a faster rate than others causing concentration risk. It makes sense to reduce individual equity exposure to more tolerable levels on these initial extremes and look to re-enter when better reward to risk setups present themselves.

An observation is that recently when a new high is hit, there has been a period of average true range contraction and lower volatility. Lower volatility generally will mean options are relatively cheaper. For investors looking to protect downside risk during these periods, purchasing put options for protection is one strategy, while a neutral option strategy may also be considered to capture some upside.

3. How do we make investments with the information we have discovered from points 1 & 2?

Considering equity returns of ATH versus non-ATH data, the distributions of returns are very similar. This implies that historically, the market does not behave that much differently when it is at an ATH. Based on this information, an investor may choose to ignore the price level of the index and invest as they would normally.

However, analysing the situation where the S&P 500 recaptures its all-time high after a yearlong period of not making a new all-time high provides us with some more interesting statistics. Most forward returns in this instance are positive. Additionally, we have seen ATR contraction in recent times. This allows the investor to think about additional ways to gain exposure that match the market dynamics at these levels. Considering these two factors, an option strategy like the bull call spread may be good way to take advantage of the historical statistics of a positive expected return and current market dynamics of lower volatility (and hence cheaper premiums).

For investors looking to invest new money directly into shares when the market is at all-time highs, looking underneath the surface of the broader market for individual names that still present fair value and are technically strong is another prudent strategy. A fundamental screener that investors may use would be to identify the companies with the best forward earnings per share growth over the next twelve months. A technical screener could be to find companies that are trending higher, however are close to their 100 period daily moving averages.